获取所有权_住房所有权经济学深入研究

获取所有权

Note from Towards Data Science’s editors: While we allow independent authors to publish articles in accordance with our rules and guidelines, we do not endorse each author’s contribution. You should not rely on an author’s works without seeking professional advice. See our Reader Terms for details.

Towards Data Science编辑的注意事项: 尽管我们允许独立作者按照我们的 规则和指南 发表文章 ,但我们不认可每位作者的贡献。 您不应在未征求专业意见的情况下依赖作者的作品。 有关 详细信息, 请参见我们的 阅读器条款 。

Part 1 of Economics of Home Ownership Deep Dive.

房屋所有权经济学深入研究的第1部分。

介绍。 (Introduction.)

For those who have previously considered or are considering the purchase of a home, then this post is meant for you to help customize your scenarios and diligence your available options. I hope that you find the included financial model, available here (select “View Raw” or hit Download), useful as you evaluate potential home purchase options. With the help of this post and the model, you’ll better understand the costs associated with home ownership and the inherent opportunity costs of not investing down payment and ongoing maintenance costs into other assets, e.g., passive market ETFs.

对于那些以前考虑过或正在考虑购买房屋的人,那么这篇文章旨在帮助您自定义方案并尽职尽责。 我希望你找到包括财务模型, 可在这里 (选择“查看原始”或命中下载),可作为您评估潜在的购房选择。 借助本文和模型,您将更好地了解与房屋所有权相关的成本以及不将首期付款和持续维护成本投资于其他资产(例如被动市场ETF)的固有机会成本。

Given my avid interest in investing and the fact that my wife and I purchased a home in 2018, I recently revised my approach to modeling out our monthly expenses, long-term savings plan and forecasting additional funds we’ll have to allocate to our family’s investment strategies. Also, with the enduring Covid-19 situation, this topic is timely since more millennials are now considering home ownership. This is largely due to the evolving perspective many have experienced given shelter-in-place requirements, the projected migrations out of major cities to suburbs/residential areas and the increasing desire for things many homes afford, such as a yard and better WFH office space.

鉴于我对投资的浓厚兴趣以及我和妻子在2018年购买房屋的事实,我最近修改了方法,以建模每月支出,长期储蓄计划并预测我们将不得不分配给家人的额外资金投资策略。 同样,在持续的Covid-19形势下,这个话题是及时的,因为越来越多的千禧一代正在考虑拥有房屋。 这主要是由于许多人在就地避难所的要求方面不断变化的观点,预计从主要城市迁移到郊区/居民区以及对许多房屋负担得起的需求的不断增长,例如院子和更好的WFH办公空间。

In this post, I provide context and a scenario-based model that you can use to evaluate different home purchase options, including variable purchase prices, down payment amounts, and lending terms, among others. The scenario-based model has flexible inputs, allowing you to customize it based on your current income(s), monthly expenses, and your personal financial situation and investment preferences.

在本文中,我提供了上下文和基于场景的模型,您可以使用该模型来评估不同的购房选择,包括可变的购买价格,预付定金和贷款期限等。 基于方案的模型具有灵活的输入,可让您根据当前收入,每月支出以及您的个人财务状况和投资偏好来对其进行自定义。

Please note that this model does not yet account for all considerations, such as 1) whether or not you should refinance and how to evaluate multiple options there, 2) it doesn’t present a full rent versus buy analysis (I link to a helpful resource and it does factor in net recurring costs in the home ownership IRR), 3) evaluates the most common 15 and 30 year fixed but not other loan types, e.g., ARM and 4) it doesn’t account for taking on PMI (lower than 20% down payment) and eliminating PMI once loan-to-value becomes <= 80%. In true product management fashion, I’ll iterate on future posts if there’s enough interest for features like this.

请注意,此模型尚未考虑所有考虑因素,例如1)是否应进行再融资以及在那里如何评估多种选择,2)它没有提供全额租金与购买分析(我链接到一个有用的链接)资源,它确实将房屋所有权的净经常性成本(IRR)考虑在内; 3)评估最常见的15年和30年期固定利率,但不评估其他贷款类型,例如ARM和4)它不考虑承担PMI(较低低于20%的首付),并在贷款转为价值等于或低于80%时消除PMI。 以真正的产品管理方式,如果对这样的功能有足够的兴趣,我将在以后的文章中进行迭代。

Personal pain point and reason for building this scenario-based model.

个人痛苦点和建立此基于场景的模型的原因。

While there are a number of useful online resources that can help inform your home purchasing decision, some of which I’ll share in a bit, where I believe this post is unique is that it will take those analyses several steps further and can be personalized to your decision set. This initial post shares a framework for thinking through the associated opportunity costs you’ll encounter when weighing the decision to tie up equity in a home versus other potential investments. In other words, given your personal assumptions, it’ll help you forecast out what the money you didn’t put into a larger home could return in the market (or some other asset(s) of your choice); and allows you to test scenarios where you’re better/worse off with a particular home purchase versus investing your capital elsewhere.

尽管有许多有用的在线资源可以帮助您做出购房决定,但我会分享其中的一些内容,我相信这篇文章的独特之处在于它将使这些分析更进一步,并且可以个性化根据您的决定。 该初始职位分享了一个框架,供您考虑权衡将房屋净值与其他潜在投资捆绑在一起的决定时遇到的相关机会成本。 换句话说,根据您的个人假设,它可以帮助您预测未投入较大房屋的钱可以在市场(或您选择的其他一些资产)中回报多少; 并允许您测试特定情况下的购房情况,而不是在其他地方投资。

In a follow-up that I will complete based on interest in this post, my plan is to turn again to Mode Analytics (older example here). In part 2, you’d further your data science analytics and dashboard development skills, creating an interactive dashboard that charts the various scenarios your financial model generates from your personalized inputs. The model, for that future post, would generate a CSV file that can be used as a flat file data source for an interactive Mode Analytics dashboard.

在我将根据对本文的兴趣而完成的后续工作中,我的计划是再次转向Mode Analytics(在此为较早的示例 )。 在第2部分中,您将进一步提高数据科学分析和仪表板开发技能,创建一个交互式仪表板,以图表形式显示您的财务模型从个性化输入生成的各种方案。 该模型将在以后的帖子中生成一个CSV文件,该文件可用作交互式Mode Analytics仪表板的平面文件数据源。

In tandem with this post, my other related articles that talk further about establishing an investment system by leveraging Python include:

与这篇文章配合使用,我的其他相关文章进一步探讨了如何利用Python建立投资系统,包括:

Part 1: Extract financial time series data from Yahoo! Finance API in Jupyter notebook;

第1部分:从Yahoo!中提取财务时间序列数据 Jupyter笔记本中的Finance API;

Part 2: Extend Part 1’s analyses and visualizations by providing the code needed to take the data sets generated and visualize them in a Dash by Plotly (Dash) web app;

第2部分:通过提供获取生成的数据集并在Dash by Plotly(Dash)Web应用程序中将其可视化所需的代码,扩展第1部分的分析和可视化;

Part 3: Build on the Stock Portfolio Analyses and Dash by Plotly approaches to understand your total shareholder return (TSR), including dividends, and track Robo Advisor-like Portfolios.

第3部分:利用Plotly方法进行股票投资组合分析和破折号,以了解您的股东总回报(TSR)(包括股息),并跟踪类似Robo Advisor的投资组合。

Disclosure: Nothing in this post should be considered investment advice. Past performance is not necessarily indicative of future returns. I am writing about generalized examples and show how to evaluate home purchase scenarios and the relative opportunity cost to allocating some/all of this capital to other investment opportunities. You should direct all investment related questions that you have to your financial advisor and perform your own due diligence on any investments mentioned in this post. Therefore, I assume no liability for any losses that may be sustained by the use of the method described in this post, and any such liability is hereby expressly disclaimed.

披露:这篇文章中的任何内容都不应视为投资建议。 过去的表现并不一定表示未来的回报。 我正在写一些通用的示例,并说明如何评估购房方案和相对机会成本,以将部分/全部资本分配给其他投资机会。 您应该将所有与投资有关的问题导向财务顾问,并对本文中提到的任何投资进行尽职调查。 因此,对于使用此职位中描述的方法可能遭受的任何损失,我不承担任何责任,特此明确声明不承担任何此类责任。

变得更聪明的房屋所有权经济学。 (Becoming Smarter on Home Ownership Economics.)

As mentioned in the intro, there are four limitations (I’m aware of) to my approach: 1) does not evaluate refinancings, 2) no full rent versus buy analysis, 3) looks exclusively at fixed rate mortgages (e.g., 15 and 30 year) and 4) model doesn’t account for PMI scenarios. Below I share resources that address #s 1 and 2. If #4 becomes of interest based on feedback, then I’ll look to update the model to incorporate PMI. My personal situation has not involved PMI, but this decision is personal and if people need additional guidance here, I’ll re-evaluate.

正如介绍中所提到的,我的方法有四个局限性(我知道):1)不评估再融资; 2)没有全额租金与购买分析; 3)只看固定利率抵押贷款(例如15和30年)和4)模型不考虑PMI情况。 下面,我分享地址#1和2的资源。如果根据反馈对#4感兴趣,那么我将寻求更新模型以合并PMI。 我的个人情况并未涉及PMI,但此决定是个人决定,如果人们在这里需要其他指导,我将进行重新评估。

Refinance evaluations. I really enjoy Zillow’s tools across the board and have found their refinancing calculator to be helpful, at a high level, as I’ve evaluated potential refinancings. As general guidance, the short form rule of thumb is to understand what your closing costs are, aka what are you being charged to complete the refinancing; let’s say those are $2k. Then look at your monthly savings versus current monthly payment; let’s say that’s $100 per month. This means it would take you ~20 months ($2k / $100 savings per month) to earn back your upfront costs on the refinancing. Needless to say, you should stay in your house for more than 20 months for this to start to make sense.

财务评估。 我非常喜欢Zillow的所有工具,并且发现了他们的再融资计算器 ,从较高的角度来看,它对我很有帮助,因为我已经评估了潜在的再融资。 作为一般指导,简短的经验法则是了解您的结算费用,也就是完成再融资所要支付的费用; 假设这些是$ 2k。 然后查看您的每月储蓄与当前的每月付款; 假设每月$ 100。 这意味着您需要约20个月的时间(每月2k美元/每月节省100美元)来赚回您的前期融资费用。 不用说,您应该在屋子里呆20个月以上,这样才有意义。

Rent versus Buy. In considering renting versus buying, I believe Travis Devitt put together a helpful resource on this, which formed some of my thinking and helped me be much smarter about the considerations: link to Travis’s tweet.

租与买。 在考虑租用还是购买时,我相信Travis Devitt在此方面提供了有用的资源,这形成了我的一些想法,并帮助我更加智能化了注意事项: 链接到Travis的推文 。

Resources. Before you get started with the model in this post, I’d encourage you to read through the first two resources below to have a much better handle on the economics of and path to home ownership. Of note, the Betterment post is extremely detailed and helpful; I’ve based several of my model’s base case assumptions using data directly from this post. The last resource presents data and addresses head on the home ownership gap that persists in America. I’m unfortunately not an expert and do not have all of the answers, but I’m willing to contribute to causes and provide help/answers where I can to support closing this gap. Please feel free to reach out to me on Twitter, @kevinboller, or leave a response to this post, if there’s a cause you recommend I look into or a question that I can help answer on the topic of home ownership.

资源。 在您开始使用本文中的模型之前,我建议您通读下面的前两个资源,以更好地掌握房屋所有权的经济性和发展途径。 值得注意的是,Betterment帖子非常详细且很有帮助; 我已经使用直接来自此帖子的数据建立了模型的几个基本案例假设。 最后一个资源提供了数据并着眼于解决美国仍然存在的房屋所有权缺口。 不幸的是,我不是专家,也没有所有答案,但是我愿意为原因做贡献,并在能够支持的地方提供帮助/答案。 如果有您建议我调查的原因或可以帮助回答有关房屋所有权的问题,请随时在Twitter上与我联系, @ kevinboller或对本帖子进行回复。

Wealthfront Home Planning Guide.

《财富前线家庭计划指南》 。

Betterment — is buying a home a good investment?

改善-购房是否是一笔好投资?

Article on home ownership gap in America.

关于美国房屋所有权差距的文章 。

使用基于场景的模型。 (Using the Scenario-based model.)

输入工作表。 (Inputs worksheet.)

When you open up the model, you will start on the Inputs worksheet that drives the rest of the formulas throughout. The schedule on the Monthly Model sheet provides a 10-year forecast. You can certainly extend this further if you would like, but it’s hard for me to believe that the average person is making a 30-year decision and I prefer to evaluate shorter time periods; this is particularly because all models are wrong and trying to model out the next 30 years is likely even more wrong than the next 10.

打开模型时,您将从“输入”工作表开始,该工作表将驱动其余的整个公式。 每月模型表上的时间表提供了10年的预测。 如果您愿意,您当然可以进一步扩展,但是我很难相信普通人会做出30年的决定,而我更喜欢评估较短的时间段。 这尤其是因为所有模型都是错误的 ,因此尝试对未来30年进行建模可能比接下来的10年更加错误。

Cell C2 on the Inputs sheet is the most important cell in the entire model. Everything in column C on this sheet should also not be modified, as the inputs will fill in based on the selected scenario, chosen in C2, which pulls from column 1 to n columns away from column C. In the columns to the right of column C, and you can add more scenarios to the right if you’d like, you change the assumptions based on the scenarios that you’re evaluating. Note that any cells in blue font mean that they can be modified, and any cells in black font should not be since they’re formula based and are scenario agnostic. While the provided scenarios are all positive cases, e.g., 3.2% home appreciation, you can certainly evaluate the same scenario multiple different ways. For example, maybe you want to compare a base scenario of 3.2% annual house appreciation and 7% annual investment returns versus 0% housing appreciation and 4% investment growth to see the impact over time to your adjusted net worth.

“输入”页面上的单元格C2是整个模型中最重要的单元格。 此表上C列中的所有内容也不应修改,因为输入将基于在C2中选择的所选方案填充,该场景将从C列的第1列拉至n列。在该列的右侧C,然后可以在右侧添加更多方案,然后根据要评估的方案更改假设。 请注意,任何蓝色字体的单元格都可以对其进行修改,而任何黑色字体的单元格都不应基于公式,并且与场景无关。 虽然所提供的方案都是积极的情况,例如3.2%的房屋增值,但您当然可以通过多种不同方式评估同一方案。 例如,您可能想比较一个基本情景,即每年房屋增值3.2%和年度投资回报7%,将房屋增值0%和投资增长率4%进行比较,以了解一段时间后对调整后的净资产的影响。

Key point: always be cognizant that when you make any adjustments to scenarios 1–4, you should always go back and cycle through the scenarios in cell C2 — type 1, 2, 3, 4 into C2 in order to cycle through these scenarios and have their inputs flow through the model; this will become evident once you get use to the remaining worksheets.

关键点:始终意识到,当您对场景1-4进行任何调整时,您应该始终返回并循环浏览单元格C2中的场景-将类型1,2,3,4输入到C2中,以便在这些场景中进行循环。让他们的输入流经模型; 一旦您习惯了其余的工作表,这一点将变得显而易见。

The Home Purchase Details and Loan Details sections, if you’ve read the resources noted above, should be straightforward. In columns D — G, I’ve included 4 templated scenarios. Income and Expenses have placeholder values and should be adjusted to reflect your personal income and expenses. I would put in after-tax income figures so that you have a better-estimated proxy for what your cash flow will be after servicing your monthly expenses; and the capital that you’ll have available to invest after those expenses are serviced. For the remaining expenses after HOA, such as home maintenance, I’d recommend leaving those as is since they’re based on the Betterment post’s data. Same recommendation for the Home Sale Inputs assumptions, including selling and closing costs.

自置居所 的个人资料和贷款细节部分,如果你读过上面提到的资源,应该直截了当。 在D到G列中,我包括4个模板化方案。 收入和支出具有占位符值,应进行调整以反映您的个人收入和支出。 我将输入税后收入数字,以便为您提供一个更好估计的代理,以说明在偿还每月支出后的现金流量; 以及支付这些费用后您将可用于投资的资本。 对于HOA之后的剩余费用,例如房屋维护,我建议将这些费用保持不变,因为它们基于Betterment帖子的数据。 对于“房屋销售投入”假设(包括销售和交易成本)也具有相同的建议。

For the Investment Performance, % of excess cash invested means that, for the money you retain post paying your monthly expenses, how much of that will you invest into a passive ETF, stocks, etc. You then must make an estimate on your nominal return, which I’ve set at 7%. You can choose to be more/less aggressive than this. Your available cash reserve, which you likely would not need, is money set aside in the event that you need more cash to support expenses in a given month (expenses exceed income); you might do this if your monthly expenses exceed your income but you manage cash flow during the year anticipating lumpier cash inflows, e.g., RSU vests twice per year; but this is not necessarily advisable or likely applicable to most.

对于投资业绩 ,所投入的多余现金的百分比表示,用于保留您每月支付的费用后,您将向被动式ETF,股票等投资多少资金。然后,您必须估算名义收益,我将其设置为7%。 您可以选择比这个更具侵略性。 您可能不需要的可用现金储备是在您需要更多现金来支付给定月份的支出(支出超过收入)时预留的资金; 如果您的每月支出超出收入,则可以执行此操作,但您可以在一年中管理现金流,以预测较大的现金流入,例如,RSU每年归属两次; 但这不一定是可取的,或可能适用于大多数人。

Net Worth Inputs, the last section, is how you’ll directly compare your home investment and other investments across scenarios to see the impact on your net worth. Again, the annual home appreciation of 3.2% is a Betterment post assumption. The down payment opportunity cost means, in scenarios where you pay a larger down payment than the base scenario (always have base in column D), we’ll deduct what that capital would’ve returned if invested elsewhere (instead of used for a larger down payment). Since the extra down payment upside is reflected in the return of the home value in the scenario where you buy a larger home and/or pay more upfront, this will show your net return relative to base. It should also make all scenarios apples-to-apples when comparing across scenarios with higher upfront home costs.

最后一部分是净值输入 ,您将如何直接比较各种方案中的房屋投资和其他投资,以查看对您的净资产的影响。 再次,3.2%的年度房屋增值是改善后的假设。 首付机会成本意味着,在您支付的首付款比基本情形大的情况下(总是在D列中有基数),我们将扣除如果将其投资到其他地方而获得的资本回报(而不是用于更大的首付)。 在您购买较大房屋和/或支付更多前期费用的情况下,由于额外的首付上行空间反映在房屋价值的回报中,因此这将显示相对于基准的净回报。 在比较具有较高前期房屋成本的各种情况时,它还应该使所有情况变得一清二楚。

每月模型工作表。 (Monthly Model worksheet.)

In cell C1, you’ll see the current scenario being evaluated based on the scenario you’ve input into C2 on the Inputs worksheet. This model shows a monthly breakdown across 10 years, and also rolls these up to annual totals for those 10 years. Row 37 shows net operating profit pre-tax, which takes your post tax income and deducts your monthly expenses. While I recommend income to be entered post-tax, the spreadsheet cannot account for your actual tax scenario; therefore I’ve called it pre-tax as further adjustments will occur when you file/pay taxes. Below this is your debt paydown (rows 45–49) and a schedule that goes through what excess cash will be invested, the projected returns from those investments, and the cash reserve (money not invested) that will build over time.

在单元格C1中,您将看到正在基于“输入”工作表上输入到C2中的方案评估当前方案。 该模型显示了10年内的每月细目,并将这些汇总到这10年中的年度总计。 第37行显示了税前净营业利润,该收入扣除了您的税后收入并减去了每月支出。 虽然我建议在税后输入收入,但电子表格无法说明您的实际税收情况; 因此,我将其称为“税前”,因为在您提交/缴税时会进行进一步的调整。 在此之下是您的债务偿还额(第45-49行)以及一个计划,该计划将分析将要投资的过量现金,这些投资的预期收益以及随着时间的推移而建立的现金储备(未投资的货币)。

You’ll see in rows 65–67 the buildup of your investable cash over time. For relevant higher cost scenarios, the opportunity cost for what you could have returned by buying a smaller home/making a smaller down payment will also accrue value over time in the same manner. It’s important to note that the investment returns in this model offer a simplified, linear view of your money growing over time. No investment will grow linearly at your annual expected return divided by 12 months; further, since this is exhibiting a dollar cost averaging approach, where you invest when you have available capital on a monthly basis, your actual returns will exhibit more volatility than the simplified model framework. Regardless, you shouldn’t get bogged down in the monthly returns and recognize that 1) you will, on average, see this appreciation annually in your investable assets (home and ETFs, et al) and 2) this model is intended to help you take a longer-term view. Ideally, given the friction in transaction and closing costs, you’ll provide yourself with 5 to 10 years in your home before deciding on moving/buying a different home.

您会在第65-67行看到随着时间的推移可投资现金的积累。 对于相关的较高成本方案,通过购买较小的房屋/进行较小的首付而可能获得的回报的机会成本也将以相同的方式随着时间的推移而增加价值。 重要的是要注意,此模型中的投资回报为您的资金随时间增长提供了简化的线性视图。 您的年度预期收益除以12个月后,任何投资都不会线性增长; 此外,由于这体现了美元成本平均法,即您每月有可用资本时进行投资,因此实际收益将比简化模型框架具有更大的波动性。 无论如何,您不应该为月度收益感到困惑,并认识到1)您平均每年会在可投资资产(房屋和ETF等)中看到这种升值,以及2)此模型旨在为您提供帮助从长远来看。 理想情况下,考虑到交易和交易成本的摩擦,在决定搬家/购买其他房屋之前,您需要在家里呆5至10年。

Net Worth over Time first evaluates the build up in home equity. This is driven off the input to annual home appreciation (which is adjusted to a monthly rate of increase in Inputs) and the paydown in debt based on the terms of the mortgage. To finalize the net worth calculation, the upside the additional down payment would’ve generated in scenarios beyond base scenario is deducted, investment growth is added and you can manually input any additional assets and liabilities that you’d like. My personal model schedule is more detailed than this, including retirement assets (Roth, 401k, etc.). When ready, you should consider building those into your model if you’d like a complete picture of your net worth alongside the projected contributions to those accounts and related growth over time.

时间净值首先评估房屋净值的增长。 这是从年度房屋增值(已调整为每月输入增长率)调整的输入以及基于抵押条款支付的债务清算的。 为了最终确定净资产,扣除了超出基本方案的方案本应产生的额外首付的上行空间,添加了投资增长,您可以手动输入所需的任何其他资产和负债。 我的个人模型时间表比这更详细,包括退休资产(Roth,401k等)。 准备就绪后,如果您希望对自己的净资产有完整的了解,并随着时间的推移对这些帐户的预计贡献和相关增长,则应考虑将其纳入模型。

While home equity grows over time, increasing your overall net worth, the Betterment article does a good job of highlighting the “problems with calculating investment returns”. For sake of brevity, there are three core drivers, in addition to home appreciation, that impact your return on home investment: 1) transaction costs, 2) cash flows, including ongoing costs (note, these are reflected in our model, see row 49 on Inputs worksheet), and leverage, aka a mortgage, increasing gains to the upside but also increasing risk on the downside. As a result, to see a true apples-to-apples comparison, in the Charts and the Recurring Costs + IRR worksheets, we’ll see how you’ll need to deduct estimated transaction costs in order to reflect your true net worth and your home investment’s projected IRR.

尽管房屋净值随着时间的增长而增长,从而增加了您的整体净资产,但Betterment文章很好地强调了“计算投资回报的问题”。 为简洁起见,除了房屋升值外,还有三个主要驱动因素会影响您的房屋投资回报:1)交易成本,2)现金流量,包括持续成本(请注意,这些都反映在我们的模型中,请参见行投入工作表上的第49页),也称为抵押贷款,既增加了上行收益,也增加了下行风险。 因此,要在图表和“经常性费用+ IRR”工作表中看到真正的比较,我们将看到您需要如何扣除估计的交易费用才能反映您的真实净资产和房屋投资的预期内部收益率。

图表工作表。 (Charts worksheet.)

On the Charts worksheet, we compare a few core metrics across scenarios over the first 5 year period. Extending this to 10 years, or beyond if you extend the model further, should be straightforward if you have some familiarity with developing and extending models.

在“图表”工作表上,我们比较了前五年中跨场景的一些核心指标。 如果您对模型的开发和扩展有所了解,那么将其扩展到10年甚至更长时间(如果您进一步扩展模型)应该很简单。

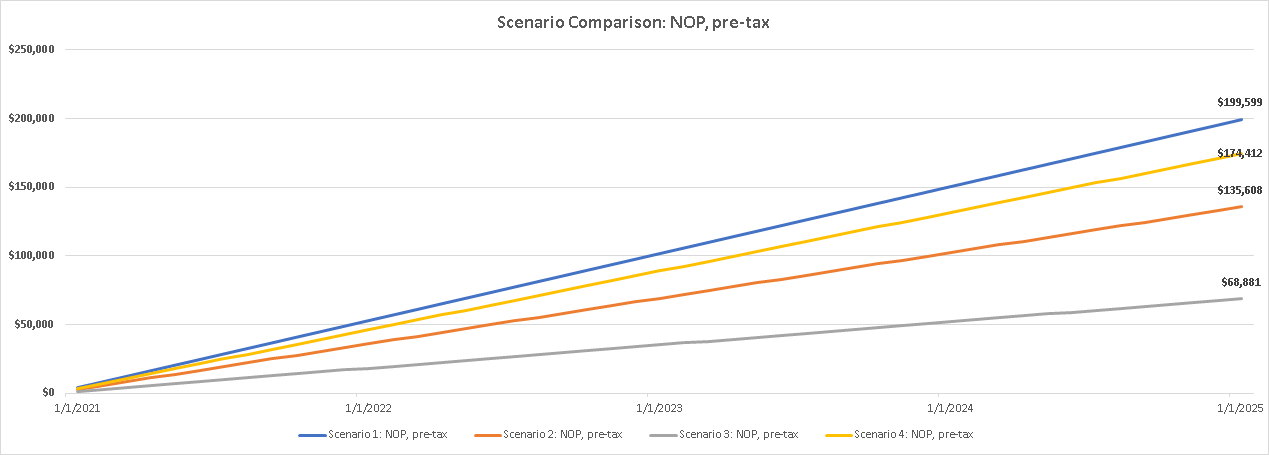

In the first chart, we compare your projected net operating profit (NOP, income less expenses) across scenarios. You can see in this case that NOP is greatest in scenario 1 and second highest in scenario 4. In scenario 4, you’ve elected to pay for the same home as scenario 1, but you’ve selected a 15-year mortgage over a 30-year one. To each their own, but I subscribe to Ric Edelman’s theory of having a 30-year mortgage — I prefer greater liquidity and diversification. Using these scenarios, you can see in Scenario 2 that you’ll have ~70% of the NOP you have in scenario 1, and in Scenario 3 you have ~35% of the NOP you would’ve had in Scenario 1 (in this scenario, you bought a home 3x as expensive as Scenario 1).

在第一个图表中,我们比较了您在各种情况下的预计净营业利润(NOP,收入减去支出)。 在这种情况下,您可以看到方案1的NOP最大,方案4的第二高。在方案4中,您选择支付与方案1相同的房屋,但是您选择了15年期抵押30年之一。 每个人都有自己的看法 ,但我赞成里德•埃德曼(Ric Edelman)的30年期抵押贷款理论 -我更喜欢更大的流动性和多元化。 使用这些方案,您可以在方案2中看到方案1中拥有约70%的NOP,在方案3中,您具有方案1中拥有的NOP约35%(在本示例中)情况下,您购买的房屋价格是情况1的3倍。

In the second chart, go to cell K101, the chart shows investment details for the selected scenario, and the table below breaks down the scenarios head to head. Given the linearity of returns and the same assumptions regarding how much is invested (80%), you’ll see that your total investment balance + excess cash for the scenarios past #1 will mirror the differences in NOP between scenarios. You can decide if you’d like to modify the scenarios’ assumptions; for example, if you buy a smaller home, maybe you’ll allocate more of your capital to investing (90%?) and/or be more aggressive with your other investments, expecting a return higher than 7%.

在第二张图表中,转到单元格K101,该图表显示了所选方案的投资明细,下表对这些方案进行了详细的分类。 鉴于收益的线性和关于投资多少的相同假设(80%),您将看到在#1之后的方案中,总投资余额+多余现金将反映方案之间NOP的差异。 您可以决定是否要修改方案的假设。 例如,如果您购买较小的房屋,也许您会把更多的资金用于投资(90%?)和/或对其他投资更具攻击性,期望收益高于7%。

In the 3rd chart, go to J160, you’ll see your net worth over time and your debt paydown over time on the secondary y-axis. For the first three scenarios, the existing loan balance as a % of original mortgage, and home equity as a part of home valuation are relatively in-line. The only difference is that I’ve assumed modestly higher interest rates for larger home purchases/greater amount borrowed. You’ll also see that your home equity reflects 30% of your net worth in scenario 1, increasing to ~60% and 90%+ in scenarios 2 and 3, and arriving at 40% in scenario 4 (where you’ve elected a 15-year mortgage; higher than scenario 1 given this). While you might conclude in column O (cell 0160) that you’re indifferent across scenarios and your net worth is relatively the same, this is not entirely correct. After deducting for projected closing costs (see U161), which estimates the net realized value you could get from the sale of your home, you see that, after 5 years, scenarios 2 and 3 actually trail scenario 1 for your adjusted net worth; whereas you’re effectively in the same spot in scenarios 1 and 4 (same purchase, different mortgage duration). The near tie between scenarios 1 and 4 indicates that, based on your investment opportunity set, you’re relatively indifferent to investing more in your home (shorter duration mortgage) versus in a diversified ETF (assuming a 7% annualized return) — tax consequences, such as deductions for mortgage interest or taxes on dividends, have not been considered for this framework but could impact this comparison. For final details on how to evaluate your potential home investment’s returns, we’ll go to our last worksheet.

在第三个图表中,转到J160,您将在次级y轴上看到随着时间的推移的净资产和随着时间推移的债务偿还。 对于前三个方案,现有贷款余额占原始抵押贷款的百分比,而房屋净值作为房屋估值的一部分,则相对较为合理。 唯一的区别是,我假设购房量较大/借入的金额较大时,利率会适度提高。 您还将看到,您的房屋净值在方案1中反映了30%的净资产,在方案2和3中分别增加至〜60%和90%+,在方案4中达到40%(您选择了15年抵押;比这种情况高出方案1)。 尽管您可能在O列(单元0160)中得出结论,您对各种情况都漠不关心,并且您的净资产相对相同,但这并不完全正确。 扣除预计的结账成本(请参阅U161)后,该成本估算了您可以从出售房屋中获得的净变现价值,您会发现,经过5年的调整后的净值,方案2和3实际上落后于方案1; 而您在方案1和4(相同的购买,不同的抵押期限)中实际上处于同一位置。 方案1和方案4之间的关系十分紧密,这表明,根据您的投资机会集,相对而言,您相对于投资于更多的房屋(较短的抵押期)而言,相对于分散的ETF(假设年化收益为7%),相对而言没有税收的后果,例如抵押贷款利息或股息税的扣除额,尚未在此框架中考虑,但可能会影响此比较。 有关如何评估潜在房屋投资回报的最终详细信息,我们将转到上一个工作表。

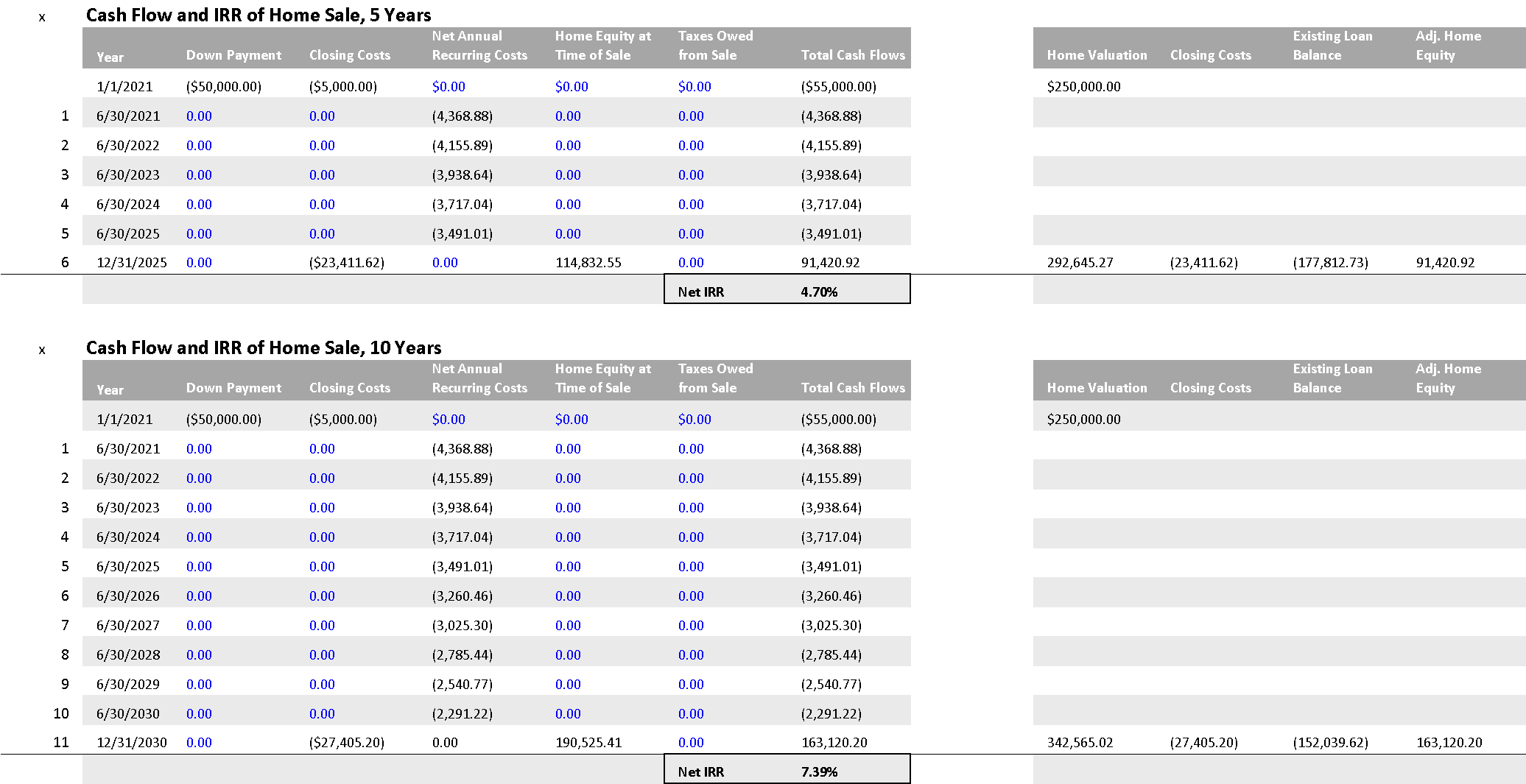

经常性费用+ IRR工作表。 (Recurring Costs + IRR worksheet.)

As stated before, the Betterment article is well detailed and very helpful to become more knowledgeable on the mechanics and implications of home ownership. However, after reading the article, you’ll still not have a way to customize the learnings to your personal situation or decision set. Given that I agreed with the author’s approach to returns, I’ve re-created two of the tables in that post within my last worksheet. The benefit is that you’ll be able to tweak scenarios and inputs and they’ll flow through these tables based on the same structure as that post.

如前所述,Betterment文章非常详细,对使人们对房屋所有权的机制和含义有更多的了解非常有帮助。 但是,阅读本文后,您仍然无法根据自己的情况或决策制定自定义的学习内容。 鉴于我同意作者的退货方法,所以我在上一个工作表中重新创建了该帖子中的两个表。 好处是您将能够调整方案和输入,并且它们将基于与该帖子相同的结构在这些表中流动。

In the Annual Recurring Costs of Home Ownership table, this lays out how to calculate net annual recurring costs (rent versus buy) for the particular scenario that you’re evaluating. For detail on this, see Ongoing Costs of Home Ownership in the Betterment post. Since this may raise questions, I’ll point out a difference between the model in my post and the table from the Betterment one. In the Betterment table, annual property taxes grow with the value of the home and homeowner’s insurance grows at inflation. While this is more accurate, I’ve left each scenario’s fully loaded monthly mortgage payment (including property taxes and insurance) constant over the model’s 10 year forecast. This is to reduce cognitive overload for what we’re covering and to make it easier to understand this model relative to online mortgage calculators and estimated payments. Since I do not grow property taxes and insurance modestly over time, this means the home ownership returns are slightly overstated; however, since this is done equally across scenarios, I believe this has an immaterial impact on your evaluation. To highlight the minimal difference, you’ll notice in the Betterment post’s Annual Recurring Costs Of Homeownership table that, after 10 years, annual property taxes and home insurance costs on a $250k home purchase only increase by ~$500 and $200, respectively.

在“房屋拥有权的年度经常性成本”表中,这列出了如何为您要评估的特定方案计算净年度经常性成本(租金与购买)。 有关此详细信息,请参见“改善”一文中的房屋自有住房成本。 由于这可能会引起问题,因此我将指出我的帖子中的模型与“改进”中的表格之间的区别。 在“改善”表中,年度财产税随着房屋价值的增长而增长,而房主的保险则随着通货膨胀而增长。 虽然这更准确,但我保留了每种方案在模型10年预测中的每月满负荷按揭付款(包括财产税和保险)不变。 这是为了减少我们所涵盖内容的认知负担,并使相对于在线抵押贷款计算器和估计付款的此模型更易于理解。 由于我不会随着时间的推移适度增加财产税和保险,因此这意味着房屋所有权回报被高估了; 但是,由于在各种情况下均可以做到这一点,因此我认为这对您的评估没有实质性影响。 为了强调最小的差异,您会在Betterment帖子的“ 年度房屋经常性成本”表中注意到,十年后,25万美元购房的年度财产税和房屋保险成本仅分别增加了约500美元和200美元。

I also show two IRR schedules, one for a five year investment horizon and the other for a ten year investment horizon. You’ll notice that the IRR is highest for scenario 4, where you pay the lowest upfront down payment (same as scenario 1) and you pay down your loan faster due to having a 15-year versus a 30-year mortgage. In this case, while your net annual recurring costs are higher in scenario 4 versus scenario 1, the greater equity value you’ve generated through paying down more of the debt principal drives the higher IRR. This exhibits the upside of the levered return from home ownership when you are able to benefit from home value appreciation.

我还显示了两个IRR计划,一个用于五年投资期,另一个用于十年投资期。 您会注意到,方案4的IRR最高,其中您支付的预付款最低(与方案1相同),并且由于有15年期抵押和30年期抵押,因此还清了您的贷款。 在这种情况下,虽然方案4的年度经常性费用净额高于方案1,但您通过偿还更多的债务本金而产生的更高的股权价值会带来更高的内部收益率。 当您能够从房屋价值升值中受益时,这显示了从房屋所有权中获得杠杆回报的好处。

However, I’ve simplified some things in the annual recurring costs table, such as the annual rent saved assumption. The annual rent saved should likely be the same for all of your personalized scenarios (please feel free to reflect this in your own evaluation), but given my assumption to drive off of the mortgage payment, saved rent is actually higher in scenario 4 and the other higher cost scenarios. I’ll need to think if this can be represented differently, but the result is that scenario 4’s IRR is likely overstated. For now, I’ve left these tables as more of a generalized illustration of the return profiles across scenarios. If you would like, it should be very easy to override the formulas in columns H and I in the first table on Recurring Costs + IRR. You can just input your particular rent saved and renters insurance saved, and then grow these at inflation.

但是,我已经简化了年度经常性费用表中的某些内容,例如节省了年度租金的假设。 在您所有个性化的方案中,节省的年租金可能应该是相同的(请随时在您自己的评估中反映出来),但是鉴于我假设不使用抵押贷款,在方案4中节省的租金实际上更高,其他较高成本的方案。 我需要考虑是否可以用不同的方式表示,但是结果是方案4的IRR可能被高估了。 现在,我将这些表留作更多情况下跨方案收益概况的概括说明。 如果愿意,可以很容易地覆盖“重复成本+ IRR”第一个表中的H和I列中的公式。 您只需输入您节省的特定租金和保存的房客保险,然后在通货膨胀时增加它们即可。

As expected, Scenarios 2 and 3 have modestly lower IRRs than Scenario 1, since you see the same price appreciation as in Scenario 1, slightly slower debt paydown due to greater interest costs and your net annual recurring costs are higher given the higher mortgage payments. Last, similar to the Betterment post, you see that the returns improve over a longer holding period (10 years versus 5), as it takes time to recoup your upfront closing costs from purchasing the home.

不出所料,方案2和3的内部收益率略低于方案1,因为您看到与方案1相同的价格升值,这归因于利息成本的增加,债务还款速度稍慢,并且由于抵押贷款的支付增加,您的年度净经常性成本也更高。 最后,类似于Betterment帖子,您会看到在较长的持有期(10年对5年)中,收益有所提高,因为需要花费时间来弥补购房所产生的前期结账成本。

I’d finally note that this model does not present an overall returns analysis across your entire set of assets; and the home ownership IRR is done independently on the final worksheet. My advice here is to focus less on returns but on the outcome that generates the highest adjusted net worth, while balancing the risk you’re comfortable taking to achieve this adjusted net worth. This is a more complicated topic and I’ll consider following up more on this if there is related feedback and questions.

最后,我要指出的是,该模型并未对您的整个资产集进行整体收益分析。 房屋所有权IRR在最终工作表上独立完成。 我在这里的建议是,将注意力集中在产生最高调整后净值的结果上,而不是着眼于收益,同时平衡您愿意承担的获得调整后净值的风险。 这是一个更复杂的主题,如果有相关的反馈和问题,我将考虑进一步跟进。

结论。 (Conclusion.)

To conclude this post, I hope that you find this framework useful in evaluating your personal opportunity set in terms of potential homes to buy, related purchase prices and key variables such as % down payment, mortgage interest rates and loan duration. While I’ve pointed to very helpful resources that I found to better understand the economics of home ownership, I’ve not found another resource that 1) personalizes monthly cash flows, 2) forecasts your build up of net worth over time, including home equity, and 3) provides a customized schedule to evaluate potential investment returns, opportunity cost, and your home’s potential IRR.

结束语,我希望您发现此框架可用于根据潜在的购房,相关的购买价格和关键变量(例如首付百分比,抵押贷款利率和贷款期限)评估您的个人机会。 尽管我指出了非常有用的资源,可以更好地理解房屋所有权的经济性,但我找不到其他资源可以1)个性化每月现金流量,2)预测随着时间的推移,包括房屋在内的净资产积累3)提供了定制的时间表,以评估潜在的投资回报,机会成本和房屋的潜在内部收益率。

The scenarios in this model largely conclude similar findings to those in the Betterment post. It takes on average 4–5 years to break-even on your closing costs, and a home can potentially be a sound investment and even exhibit a comparable return profile to a total stock market ETF (such as Vanguard’s VTI). This will not always be the case and the Betterment post does a good job of highlighting where things can go wrong.

该模型中的场景在很大程度上得出了与“改善”职位相似的结论。 收支成本平均需要4到5年的时间才能达到收支平衡,而房屋可能是一项可靠的投资,甚至表现出与整个股票市场ETF(例如Vanguard的VTI )相当的回报率。 情况并非总是如此,Betterment职位可以很好地突出出现问题的地方。

In combination with the resources I’ve linked to, now that you have a customizable model that allows you to evaluate your decision set across your housing and investment opportunities, you should feel fully informed that you’ll make a well researched decision and step into home ownership with your eyes wide open. In doing so, I believe that owning a home can be a great place to be; and you’ll have a strong grasp on how it fits into your overall personal finances and your forecasted investment and retirement strategy.

结合我链接到的资源,现在您有了一个可自定义的模型,该模型可让您评估住房和投资机会中的决策集,您应该充分了解自己将进行深入研究并做出正确的决定拥有房屋,睁大眼睛。 这样,我相信拥有房屋可以成为一个好地方。 并且您将对它如何适应您的整体个人财务以及预测的投资和退休策略有很强的把握。

If you enjoyed this post, it would be awesome if you would click the “claps” icon (more than once!) to let me know and to help increase circulation of my work. If you would like to leave a comment on any suggested edits, feature requests or interest in a follow-up post, please let me know that as well.

如果您喜欢这篇文章,那么如果您单击“拍手”图标(不止一次!)来告诉我并帮助增加我的作品流通量,那就太好了。 如果您想对任何建议的修改,功能要求或对后续帖子的兴趣发表评论,请也告诉我。

Feel free to also reach out to me on twitter, @kevinboller, and my personal blog can be found here. Thanks for reading!

也可以通过Twitter @kevinboller与我联系 ,也可以在此处找到我的个人博客。 谢谢阅读!

翻译自: https://towardsdatascience.com/economics-of-home-ownership-deep-dive-427fd1b17a95

获取所有权

http://www.taodudu.cc/news/show-2554584.html

相关文章:

- 【MIT 6.0001 课程笔记】Problem Set 1

- 三种最常见的框架解析 | 如何创建JUnit参数化测试

- 遇到slideUp Down 问题

- Payment相关逻辑

- 客户预付款处理和设置

- POSTING_INTERFACE_DOCUMENT解决特别总账'W'类型的过账问题

- Down Payment一个不错的练习

- 【FI-AP】预付定金处理(Down payment)

- SAP Down Payment的设置和使用

- uniapp 查看图片点击放大预览图片 单张 多张

- SQLServer2019 如何导出单张表数据

- mmdetection中使用训练好的模型单张图片推理并保存到文件夹

- 微信小程序 之wx.previewImage图片预览(单张图片预览)

- cesium添加单张图片

- Vue input[file] 原生上传 单张上传

- 使用ffmpeg命令把单张或多张图片生成固定时长的视频

- (最新)mmdetection测试单张/多张图片并保存

- 三维重建 | 单张彩色图像三维重建学习框架

- yolov5测试单张图片

- Difference between Static video and Single image ?静态视频和单张图像的区别

- 爬虫单张图片

- 怎么利用pytorch训练好的模型测试单张图片

- 单张图片生成三维点云

- 单张像片空间后方交会

- Unity Shader学习-单张纹理

- 输入单张图片到神经网络

- 三维重建 | 单张RGB图片生成三维网格模型

- 利用pytorch训练好的模型测试单张图片

- MINIST数据集手写数字识别单张图片读入测试代码

- Android Retrofit2.0 上传单张图片和多张图片

获取所有权_住房所有权经济学深入研究相关推荐

- 定制开发软件所有权_职业所有权软件开发人员指南

定制开发软件所有权 介绍 (Introduction) 您的职业正在流向大海吗? (Is Your Career Drifting Out To Sea?) Like a frog who's slo ...

- 取消管理员取得所有权_管理员所有权,教您win10怎么获得管理员所有权

win10现在发布也有很久了,而小伙伴们对它的印象与评价也越来越高.但是今天小编要说的不是它的优点,而是关于它的一个操作步骤.那就是win10要怎么获取管理员所有权.小伙伴们快和我一起来看看吧~ 我们 ...

- 取消管理员取得所有权_管理员所有权,手把手教你win10怎么获得管理员所有权

win10现在发布也有很久了,而小伙伴们对它的印象与评价也越来越高.但是今天小编要说的不是它的优点,而是关于它的一个操作步骤.那就是win10要怎么获取管理员所有权.小伙伴们快和我一起来看看吧~ 小伙 ...

- 取消管理员取得所有权_苏州即将全面取消房迁落户!有房就能落户的时代结束了!...

2020年1月1日起,苏州将全面取消房迁落户!以后落户只能通过人才引进和积分! 符合以下资格的小伙伴要抓紧时间啦: 购买市区成套商品住房75平方米以上,并于2016年12月31日前依法取得房屋所有权证 ...

- 取消管理员取得所有权_电脑系统如何取得管理员所有权

代码如下: Windows Registry Editor Version 5.00 [HKEY_CLASSES_ROOT\*\shell\runas] @="获取管理员所有权" ...

- 取消管理员取得所有权_企业取得违约补偿款是否一律应缴增值税呢?

引言: 国家税务总局深圳市税务局在回答纳税人关于违约金支出如何税前扣除的问题时,从侧面透露出不是所有情形下的违约金都属于增值税的应税范围.本文要讨论一个类似的问题,也即在合同法律关系中形成的违约补偿款 ...

- 管理员获得所有权_在Windows 7中获得注册表项的所有权

管理员获得所有权 We have previously written about how to take ownership of files and folders in Windows 7, b ...

- 经济学自身利益最大化_劳动经济学:研究劳动力市场运作的专业

多年以来同学们对劳动经济学认知上存在误区,很多同学一上来看到劳动两字会误以为这是让自己去当工人干活. 事实并非如此,例如人力资源管理,大家都知道是一门很热门.实用的管理学,毕业后可以从事hr的工作,其 ...

- 取消管理员取得所有权_利用管理员取得所有权删除顽固文件

自己的电脑,有时候卸载软件残余目录文件等竟然删不掉.哎哟哟~妈的智障哟~ 怎么能容忍,我的电脑我做主! 这里涉及到文件权限的问题,你没有权限就删不掉啦.上图提示需要管理员组来删除,注意是组. 纳尼?管 ...

- 无法打开虚拟机,获取该虚拟机的所有权失败。 主机上的某个应用程序正在使用该虚拟机。

D:\Program Files (x86)\VMwareWorkspace\henu3\henu3.vmx 在启动即可!

最新文章

- 有抱负的Web开发人员应考虑的6件事

- SQLServer之创建INSTEAD OF INSERT,UPDATE,DELETE触发器

- RabbitMQ安装和运行

- Android布局管理器-使用TableLayout表格布局管理器实现简单的用户登录页面

- mysql数据库安全审计_MySQL数据库安全日志审计工具

- 如何在内核里面查找某些结构体或者宏的定义

- Java 对象的序列化和反序列化

- Spyder打开报错解决办法

- LeetCode 1748. 唯一元素的和

- 计算机应用基础的客观题,计算机应用基础专题库客观题参考答案11

- nginx+kibana代理以及简单认证

- HashMap原理剖析

- BPE, WordPiece, SentencePiece

- C语言——输出一个正方形

- 逻辑回归和决策树_结合逻辑回归和决策树

- lol丢失base.dll文件怎么办?base.dll文件下载

- python的pyside2安装

- (0105)iOS开发之iOS13 暗黑模式(Dark Mode)适配

- jq jqprint 设置页脚_jquery web打印 取消 页眉和页脚

- 第四届高等教育国际研讨会