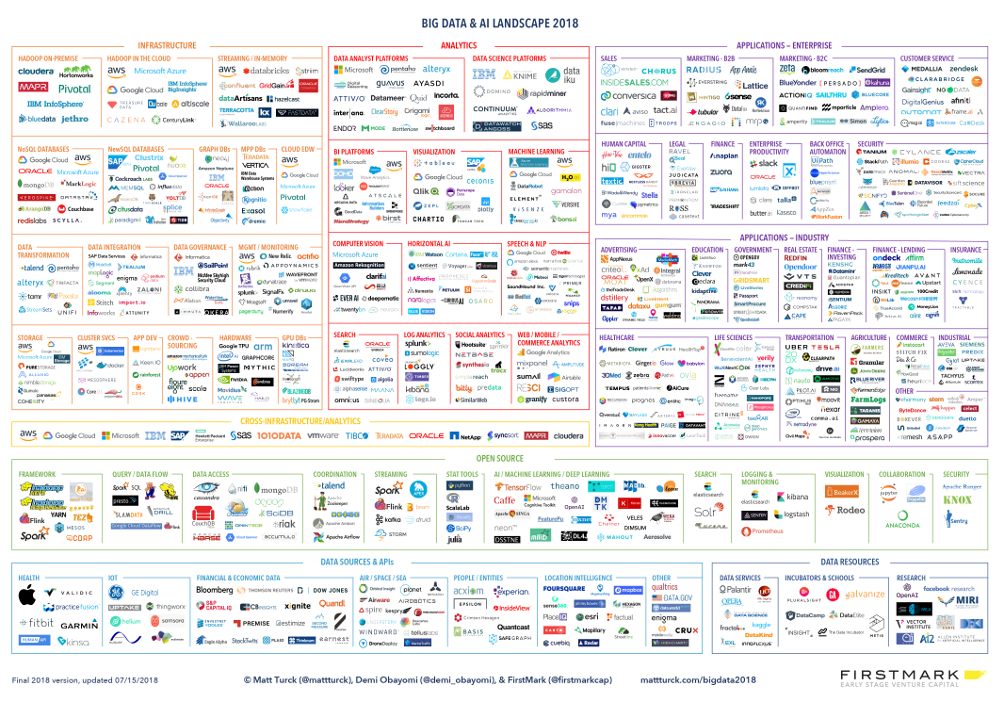

Great Power, Great Responsibility: The 2018 Big Data AI Landscape

http://mattturck.com/bigdata2018/

![]()

It’s been an exciting, but complex year in the data world.

Just as last year, the data tech ecosystem has continued to “fire on all cylinders”. If nothing else, data is probably even more front and center in 2018, in both business and personal conversations. Some of the reasons, however, have changed.

On the one hand, data technologies (Big Data, data science, machine learning, AI) continue their march forward, becoming ever more efficient, and also more widely adopted in businesses around the world. It is no accident that one of the key themes in the corporate world in 2018 so far has been “digital transformation”. The term may feel quaint to some (“isn’t that what’s been happening for the last 25 years?”), but it reflects that many of the more traditional industries and companies are now fully engaged into their journey to become truly data-driven.

On the other hand, a much broader cross-section of the public has become aware of the pitfalls of data. Whether it is through the very public debate over the risks of AI, the Cambridge Analytica scandal, the massive Equifax data breach, GDPR-related privacy discussions or reports of growing government surveillance in China, the data world has started revealing some darker, scarier undertones.

Both are the flipside of the same phenomenon, which has been brewing for many years but is now in full display: just about everything (whether personal or professional) is rapidly getting digitized, and data technologies are becoming more adept than ever at processing and analyzing this massive data exhaust, increasingly in real time. From this can result both magic and abuse. The debate on how to combine this great power with a necessary sense of responsibility has become essential.

Let’s highlight some of the key trends and events of 2018.

Infrastructure & Analytics

From an industry standpoint, the data ecosystem remains as exciting and vibrant as ever, with a rich tapestry of innovative startups, mature “scale-ups”, and many aggressive public technology vendors. Most importantly, many customers large and small are deploying those technologies in production at scale, and reaping undeniable value from their efforts.

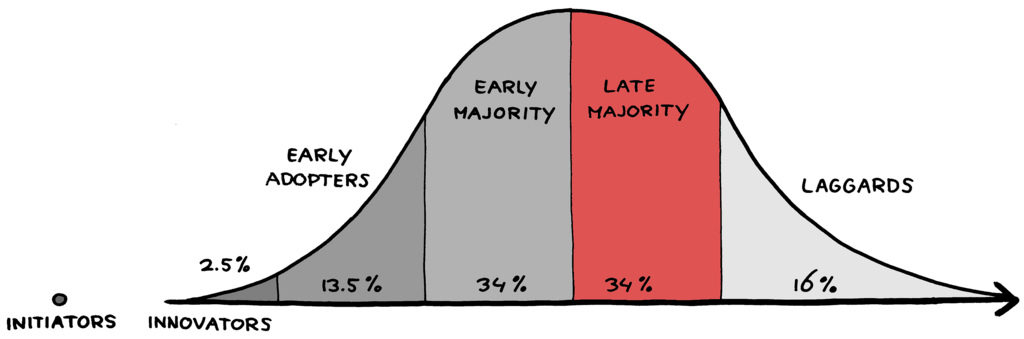

As the cycle of replacing older IT technologies with more modern data products continues, it seems that the Big Data market (infrastructure, analytics) is cycling through the early majority of buyers and transitioning into the late majority of the traditional adoption curve.

In addition, the data world continues its inexorable evolution towards the cloud. It is actually staggering to see how fast the large public cloud providers (AWS, Azure, Google Cloud Platform, IBM) are growing, considering they already each generate billions of dollars of revenues every quarter. The trend raises ongoing concerns around vendor lock-in, and this may open up opportunities for startups offering multi-cloud solutions. However, to date even companies adopting multi-cloud strategies tend to still rely on one vendor as their primary provider.

As they keep growing, large cloud providers increasingly compete with each other by offering a wide array of Big Data, data engineering and machine learning tools through their platforms (e.g., Amazon Neptune, Google AutoML, etc.) – and often with aggressive pricing, to attract more developers, as their true business model is data storage. As the scope and sophistication of such tools keep growing, this has a big impact on the data technology landscape, making it arguably harder for startups to compete, at least for broad, horizontal opportunities. A bit more every year, the list of product announcements at big annual cloud vendor conferences (see AWS re:Invent, for example) sends shockwaves in the startup industry, as they put cloud vendors in direct competition with dozens of VC-backed startups in one fell swoop. It will be interesting to see how public markets react to the upcoming Elastic IPO, an open-source software company that saw Amazon launch a direct competitor, Elasticsearch, three years ago.

Plenty of opportunities for startups remain, however, as long as they are sufficiently differentiated. Many in the space are scaling fast, and there are a number of particularly interesting, fast-growing segments in the infrastructure and analytics part of the ecosystem, including streaming/real-time, data governance, and data fabrics/virtualization. The explosion of interest in AI has also led to great opportunities (and a lot of funding) in AI chips, GPU databases, AI devops tools, and platforms enabling the deployment of data science and machine learning in the enterprise.

Machine Learning & AI

It’s certainly been a wild year in the world of AI research, with anything from the prowess of AlphaZero to the staggering pace of release of new advances – new forms of Generative Adversarial Networks, Vicarious’ new Recursive Cortical Networks, Geoff Hinton’s new Capsule Networks. AI conferences like NIPS have grown to attract 8,000 people and thousands of academic papers are being submitted every day.

At the same time, the pursuit of AGI remains elusive, perhaps thankfully so. Much of the current wave of excitement (and fear) about AI results from the impressive performance of deep learning since 2012 but, in the AI research community, there’s a growing sense of “what now?” as some question the foundations of deep learning (backpropagation) and others look to move past what they consider “brute force” approaches (lots of data, lots of computing power), perhaps in favor of more neuroscience-based approaches.

Far from fearing robot world domination, many in the AI research community are concerned that continued over-hyping of the field may eventually disappoint and lead to another AI nuclear winter.

Outside of AI research, however, we are just at the beginning of a wave of deployment and application of deep learning in the real world across a variety of problems involving speech recognition, image classification, object recognition and language, in different industries. If the infrastructure and analytics part of the ecosystem is getting to the late majority, we’re still very much in early adopter territory for enterprise and vertical AI applications.

The Cambrian explosion of deep-learning based startups that started a year or two ago has mostly continued unabated, even though the AI startup market is (arguably) showing signs of finally cooling down. Expectations, round sizes and valuations remain high, but we are certainly past the phase where big Internet companies would snap up very early AI startups at high prices just for the talent. The air is also clearing up a bit and revealing “real” AI startups, versus a number of other companies that were leveraging the hype. Some of the AI startups that were founded in the 2014-2016 time frame are starting to hit early scale, and many are offering increasingly interesting products across industries and verticals including health, finance, “industry 4.0” and back office automation. Deep learning will continue bringing a lot of value in real world applications for years to come, and vertical-focused AI startups have many great opportunities ahead of them.

This continued explosion is very much a global phenomenon, with Canada, France, Germany, the U.K. and Israel being particularly active. However, China seems to be playing at a completely different level in AI, with reports of government-led pooling of data at mind-boggling scale (across Internet companies and municipalities), rapid advances in areas such as facial recognition and AI chips, and gigantic rounds of financing for its startups: according to CB Insights, China accounted for only 9% of global AI deal share but nearly 48% of global AI funding in 2017, up from 11% in 2016 (see some examples below).

In the same vein, issues of data privacy (and ownership and security) are emerging as a major concern around the world. In the early days of the Internet, data privacy was about protecting what we did online, a comparatively small portion of our activities. Correspondingly, only a small (albeit vocal and passionate) minority of people truly cared. As just about every aspect of our personal and professional lives is now connected to the Internet through an ever increasing array of connected devices, the stakes are changing. With its ability to spot anomalies in massive data sets, predict outcomes and recognize faces, AI is compounding the data privacy problem.

A separate but related concern is that a lot of this data is owned by large Internet companies (GAFA). Some, like Facebook, have proven to be a less than perfect steward of it. Nonetheless, this data provides them an unfair advantage in the race to produce ever more powerful AI.

Against those issues, an emerging theme is to think of the blockchain as a possible foil against the risks of AI, as well as a way for others, outside of GAFA, to produce great AI. Crypto economics are viewed as a way to incentivize individuals to provide their personal data and for machine learning engineers to build models by processing this data anonymously. It all remains very experimental, but some early marketplaces and networks are emerging

The 2018 Landscape

Without further ado, here’s our 2018 landscape.

Quite semantic note: buzz terms come and go. Fewer people speak about “Big Data”, many more about “AI”, often to described the same reality. Consequently, we have slightly rebranded our 2018 landscape: it is now called the “Big Data & AI” landscape!

To see the landscape at full size, click here.

(The image is high-res and should lend itself to zooming in well, including on mobile)

To download the full-size image, click here.

To view a full list of companies in spreadsheet format, click here.

This year, my FirstMark colleague Demi Obayomi provided immense help with the landscape.

We’ve detailed some of our methodology in the notes to this post. Thoughts and suggestions welcome – please use the comment section to this post.

Who’s in, who’s out

On the exit front, the last year (since our 2017 landscape) has seen solid, but not extraordinarily strong.

A few key companies appearing on the landscape went public, in particular Cloudera, MongoDB Pivotal and Zuora. Others are preparing to go out at the time of this writing, such as Elastic.

Some notable acquisitions also occurred, including in particular Mulesoft (acquired by Salesforce post-IPO, for $6.5B), Flatiron Health (acquired by Roched for $2.1B), Appnexus (acquired by AT&T for $1.6B), Syncsort and Vision Solutions (acquired for $1.2B by Centerbridge Partners), Moat (acquired by Oracle for $850M), Integral Ad Science (acquired by Vista Equity Partners for $850M), eVestment (acquired by NASDAQ for $705M) and Kensho (acquired by S&P Global for $550M). It is worth noting that, other than Mulesoft, all those companies are headquartered on the East Coast (New York, Boston and Atlanta).

Many other companies were also acquired for smaller amounts: Gigya (SAP), Blue River Technology (Deere & Co), CoreOS (Red Hat), Guavus (Thales), Lattice Data (Apple), Socrata (Tyler Technologies) and PracticeFusion (AllScripts).

On the investment front, this was a year of big financing rounds for some Big Data and AI startups, particularly in China, with a number of oversized investments including Bytedance ($3B in total across 2 rounds in 2017), NIO ($1.6B across two rounds in 2017), and SenseTime ($850M across two around in 2017 and 2018).

Major rounds of US companies appearing on the landscape include Snowflake Computing ($263M Series A – see our recent fireside chat at Data Driven NYC), Cohesity ($250M Series D), Dataminr ($221M Series E), Affirm ($200M Series E), Rubrik ($180M Series D), Qualtrics ($180M Series C – see an older but still relevant fireside chat at Data Driven NYC), Tanium ($180M private equity round), ThoughtSpot ($145M Series D) and Coveo ($100M private equity round) and C3IoT ($100M Series F).

____________________

NOTES:

1) As every year, we couldn’t possibly fit all companies we wanted on the chart. While the general philosophy of the chart is to be as inclusive as possible, we ended up having to be somewhat selective. Our methodology is certainly imperfect, but in a nutshell, here are the main criteria:

- Everything being equal, we gave priority to companies that have reached some level of market significance. This is a reasonably easy exercise for large tech companies. For growing startups, considering the limited amounts of data available, we often used venture capital financings as a proxy for underlying market traction (again, probably imperfect). So everything else being equal, we tend to feature startups that have raised larger amounts, typically Series A and beyond.

- Occasionally, we made editorial decisions to include earlier stage startups when we thought they were particularly interesting.

- On the application front, we gave priority to companies that explicitly leverage Big Data, machine learning and AI as a key component or differentiator of their offering. As discussed in the piece, it is a tricky exercise at a time when companies are increasingly crafting their marketing around an AI message, but we did our best.

- This year as in previous years, we removed a number of companies. One key reason for removal is that the company was acquired, and not run by the acquirer as an independent company.. In some select cases, we left the acquired company as is in the chart when we felt that the brand would be preserved as a reasonably separate offering from that of the acquiring company.

2) As always, it is inevitable that we inadvertently missed some great companies in the process of putting this chart together. Did we miss yours? Feel free to add thoughts and suggestions in the comments.

3) The chart is in png format, which should preserve overall quality when zooming, including on mobile.

4) As we get a lot of requests every year: feel free to use the chart in books, conferences, presentations, etc – two obvious asks: (i) do not alter/edit the chart and (ii) please provide clear attribution (Matt Turck, Demi Obayomi and FirstMark Capital).

5) Disclaimer: I’m an investor through FirstMark in a number of companies mentioned on this Big Data Landscape, specifically: ActionIQ, Cockroach Labs, Dataiku, Frame.ai, Helium, HyperScience, Kinsa, Timber, Sense360 and x.ai. Other FirstMark portfolio companies mentioned on this chart include Bluecore, Engagio, HowGood, Payoff, Knewton, Insikt, Optimus Ride, and Tubular. I’m a small personal shareholder in Datadog.

转载于:https://www.cnblogs.com/davidwang456/articles/9415007.html

Great Power, Great Responsibility: The 2018 Big Data AI Landscape相关推荐

- 2018年的AI/ML惊喜及预测19年的走势(二)

年度回顾:2018年的AI/ML惊喜及预测19年的走势(一) Unravel Data首席执行官Kunal Agarwal 人工智能和机器学习的日益重视将会推动TensorFlow和H2O实现技术突破 ...

- 2018年ML/AI重大进展有哪些?LeCun推荐了这篇回答

乾明 编译整理 量子位 报道 | 公众号 QbitAI 回望2018,AI大潮依旧浩浩汤汤,势头不减. 这一年都有哪些重要进展呢?2018年即将过去,一些大牛也给出了自己的看法. 刚刚,前Quora技 ...

- GDPR: Impact to Your Data Management Landscape: Part 4

与欧盟的通用数据保护规定的(GDPR)1时间越来越近了.从2018年5月25日起,任何一个未能满足新法规的组织将面临高达全球收入4%的罚款,或者是2000万欧元--无论哪种罚款--任何进一步的数据 ...

- GDPR: Impact to Your Data Management Landscape: Part 2

与欧盟的通用数据保护规定的(GDPR)1时间越来越近了.从2018年5月25日起,任何一个未能满足新法规的组织将面临高达全球收入4%的罚款,或者是2000万欧元--无论哪种罚款--任何进一步的数据 ...

- GDPR: Impact to Your Data Management Landscape: Part 1

与欧盟的通用数据保护规定的(GDPR)1时间越来越近了.从2018年5月25日起,任何一个未能满足新法规的组织将面临高达全球收入4%的罚款,或者是2000万欧元--无论哪种罚款--任何进一步的数据 ...

- Data + AI Summit 2022 超清视频下载

Data + AI Summit 2022 于2022年06月27日至30日举行.本次会议是在旧金山进行,中国的小伙伴是可以在线收听的,一共为期四天,第一天是培训,后面几天才是正式会议.本次会议有超过 ...

- 年度重磅:《AI聚变:2018年优秀AI应用案例TOP 20》正式发布

2018 年,AI 行业的关键词或许非"落地"二字莫属 ,人们强烈期待着更多 AI 技术应用和深入商业化. 一方面,科技巨头们在横向铺设 AI 技术平台,但也更强调 AI 与每一个 ...

- 2018年中国AI行业研究报告

2018年中国AI行业研究报告(附下载) 核心观点: 1.广义人工智能指通过计算机实现人的头脑思维所产生的效果,是对能够从环境中获取感知并执行行动的智能体的描述和构建:相对狭义的人工智能包括人工智能产 ...

- 2018年,AI会在金融行业哪些方向上发力?

原作 Todd Clark 加州金融服务公司CO-OP的CEO Root 编译自 Payments Journal 量子位 出品 | 公众号 QbitAI 对于很多人来说,提起人工智能这个词,更多会联 ...

最新文章

- ps怎么更改背景图层大小_PS软件零基础抠图教程,教你PS滤镜抠图技巧和方法

- 【错误记录】360 加固后的运行错误 ( 加固 SO 动态库时不能对第三方动态库进行加固 )

- android自定义金额输入键盘_Android 自定义输入支付密码的软键盘实例代码

- 蓝桥杯评分标准_蓝桥杯比赛要求

- php post 丢失,php post大量数据时发现数据丢失问题解决方法,post数据丢失_PHP教程...

- 打开mysql的远程连接_开启mysql的远程访问权限

- 《面向对象程序设计》课程作业(七)

- 8运行不了_民航局暂停运行737max8,分析可能因为“它”导致飞机俯冲坠落

- day1-接口测试与接口测试工具

- 如何将PPT进行压缩?PPT压缩的方法是什么

- CSS的border属性绘制简单三角形、边框三角形

- 从零开始学USB(十五、USB的设备状态)

- 如何从macOS Catalina向iPhone添加自定义铃声

- 中国石油大学《混凝土》第二阶段在线作业

- 疾病研究:重症肌无力

- sql server获取当前日期

- 怎么能学会做买卖步骤是什么(想做买卖赚钱应该先从什么做起)

- css多个属性怎么写,.css多个属性读取写法?

- 普通程序员的出路是什么?

- 镀铬亮条怎么修复_汽车镀铬亮条生锈腐蚀怎么办如何修复